The Cash Trapped in Your Own Operations

OPERATIONAL EXCELLENCESTRATEGY & LEADERSHIPOPERATIONAL EFFECTIVENESS

6/25/2026

When a growing business needs cash — to hire ahead of demand, invest in equipment, fund a new initiative, or simply build a buffer against uncertainty — the instinct is to look outward: a line of credit, a loan, an investor. These external sources have their place. But the research consistently reveals that for most businesses, a significant pool of cash is already inside the operation, trapped in the timing of how the business converts its activities into cash — and accessible through operational discipline rather than external financing.

This trapped cash has a name in financial management: working capital tied up in the cash conversion cycle. The Hackett Group's 2025 Working Capital Survey found that $1.7 trillion remains trapped in excess working capital among just the 1,000 largest U.S. public companies — equal to 35% of their gross working capital and 11% of aggregate revenue. The same dynamic operates at every business scale. And as Post 13 of this series established, cash flow problems — not profitability problems — are the leading cause of small business failure. Working capital management is where cash flow is either protected or quietly squandered.

84% of growing companies faced a cash flow gap at least once in the past year — even profitable ones, because the cash conversion cycle was not actively managed

Visa Growth Corporates Working Capital Index, 2024–2025

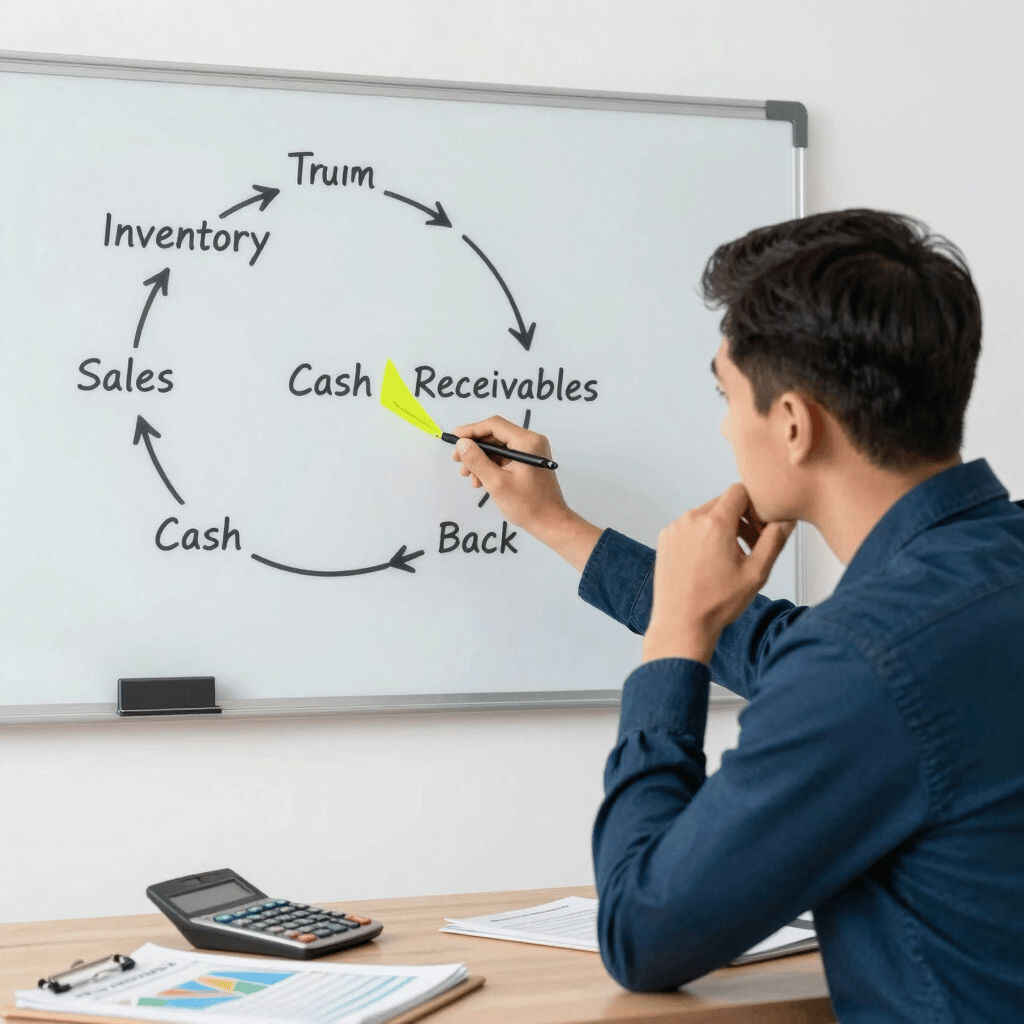

Understanding the Cash Conversion Cycle

The cash conversion cycle (CCC) measures the number of days between when a business pays for what it needs to operate and when it actually collects the cash from selling the result. It has three components, and each one is a lever a business can pull. Days Inventory Outstanding (DIO) — how long inventory sits before it's sold. Days Sales Outstanding (DSO) — how long customers take to pay after a sale. And Days Payable Outstanding (DPO) — how long the business takes to pay its own suppliers. The formula: CCC = DIO + DSO − DPO.

The shorter the cash conversion cycle, the faster the business turns its operational activity into available cash — and the less external financing it needs to fund the same level of operations. A business that collects from customers faster, holds less idle inventory, and negotiates reasonable supplier terms can fund its own growth from internal cash flow that a less disciplined competitor has to borrow.

$1.7T trapped in excess working capital among the 1,000 largest U.S. companies — 35% of gross working capital sitting idle

Hackett Group 2025 Working Capital Survey

19 vs 65 days — cash conversion cycle for a top retail/eCommerce performer vs. a top manufacturing/construction performer, showing how industry shapes the target

Visa Working Capital Index, 2024–25

73.7% of SME financial performance improvement attributable to cash management practices in one regression study of 100 SMEs

Onyango et al. SME Cash Management Research, 2023

37 days average cash conversion cycle for the largest U.S. nonfinancial companies in 2024 — a 4% improvement, showing even leaders have room

Hackett Group, 2025

The academic research underscores why this matters specifically for smaller businesses. Multiple SME studies — including Oha et al.'s 2024 analysis — found that a longer cash conversion cycle and higher inventory levels reduce profitability, while effective payables and receivables management positively influence financial performance. Onyango et al.'s regression analysis of 100 SMEs found that cash management practices accounted for 73.7% of financial performance improvements. Working capital discipline is not a treasury nicety. It is, for a small business, one of the most direct levers on both liquidity and profitability.

In an economic environment where the only certainty is uncertainty, businesses must take a proactive approach to working capital. The cash is hiding in plain sight — in inventory, in unpaid invoices, and in payment timing that no one has deliberately managed.

— The Hackett Group 2025 Working Capital Survey

The Three Levers — and How to Pull Each

1 Days Sales Outstanding: collect faster

For most service and B2B businesses, DSO is the largest and most controllable component. The cash a business has earned but not yet collected is, functionally, an interest-free loan the business is extending to its customers. Tightening it requires operational discipline rather than aggressive collections: invoice immediately on delivery rather than at month-end, define and enforce clear payment terms, automate payment reminders (Post 27), offer modest early-payment incentives where the cost is less than financing, and follow up on overdue accounts through a documented process rather than sporadic personal effort. A reduction of even ten days in DSO can free meaningful cash in a business of any size.

2 Days Inventory Outstanding: hold only what you need

For product, retail, and manufacturing businesses, inventory is often where the most cash sits trapped — and where the carrying cost quietly compounds in a higher-interest environment. Excess inventory is cash converted into goods sitting on a shelf, exposed to obsolescence, storage cost, and the opportunity cost of capital that could be deployed elsewhere. Inventory discipline — demand forecasting, identifying slow-moving stock, right-sizing reorder quantities, and eliminating the safety buffers that grew larger than the actual risk justifies — releases trapped cash directly. The research is consistent: lower DIO correlates with higher profitability across SME studies.

3 Days Payable Outstanding: pay on optimal terms, not early

Many small businesses pay suppliers faster than required — out of habit, relationship instinct, or simply the absence of a managed payables process. Paying earlier than terms require hands cash to suppliers before it's needed, shortening the time the business has use of its own money. The discipline here is balance: paying on the optimal schedule the terms allow (not late, which damages relationships and credit, but not early without reason), and where the relationship supports it, negotiating extended terms that reflect the business's value as a customer. The Hackett research found DPO improvement was the primary driver of the working capital gains that top performers captured in 2024.

Building Working Capital Visibility

The reason working capital remains an unmanaged source of trapped cash in most small businesses is not complexity — it is invisibility. The cash conversion cycle does not appear on a standard P&L. Without deliberately calculating and tracking DIO, DSO, and DPO, a business has no view of where its cash is trapped or how much could be released. Establishing these three metrics, calculating the cash conversion cycle, benchmarking against industry norms (which vary widely — 19 days for top retail performers, 65 for manufacturing), and reviewing them on a regular cadence converts working capital from an invisible drag into a managed source of internal funding.

This connects directly to the cash flow forecasting discipline of Post 13: the rolling 13-week forecast tells the business when cash will be tight, and working capital management gives it levers to address the tightness from inside the operation rather than reaching immediately for external financing. For a growing business, the cash to fund the next phase is frequently already there — earned, but not yet collected; invested, but sitting idle in inventory; paid out, but earlier than it needed to be.

Where to start

Calculate your cash conversion cycle: how many days does inventory sit (DIO), how many days until customers pay (DSO), and how many days until you pay suppliers (DPO)? CCC = DIO + DSO − DPO. That single number, tracked over time, reveals how much of your cash is trapped in operations — and each component points to a specific, actionable lever for releasing it.

Contact

Let's improve your business together.

contact@rmscsolutions.com

© 2026 All rights reserved.